Wall Street is the world’s most sophisticated misinformation machine.

Investing itself is not confusing–or at the least, it’s nowhere near as confusing as the frauds and goofballs on Wall Street’s payroll would have you believe.

Once you’ve gotten to the point where you are spending far less than you make, the last thing you want is for your invested savings to be eaten away by a bunch of hedge fund guys and two-bit salesmen. The problems with Wall Street, though, are deep. It goes way past mere greed. Wall Street isn’t just fooling you; it’s fooling itself.

So let’s get right down to it.

Part 1: No one knows nuthin’

When my investing hero, Jack Bogle, first showed up on Wall Street, he met a delivery truck driver. This working-class driver told him the truest thing that Jack ever heard while working in the belly of the beast. “Jack”, he said, “Nobody knows nuthin’.”

In particular, nobody knows anything about the future. Predictions don’t work. And we are pretty bad at predicting things, but especially bad when it comes to investments.

The key to remember with investments is this: If the economy is expected to be a 9 on a scale of one to ten, and instead it’s an 8, stock returns will be poor. On the other hand, if everyone thinks the economy is going to be a 2, and instead it’s a 3, stock returns will be great. In order to effectively predict anything in the markets, you have to do more than predict what’s going to happen. You have to predict what everyone thinks is going to happen. And what everyone thinks everyone thinks is going to happen. And what everyone thinks everyone thinks everyone thinks….

You get the idea.

And of course, we aren’t good at making predictions anyway. The book Expert Political Judgment: How Good is it, and How Can We Know? attempted to answer the question posed by its title. The author, Philip Tetlock, studied 284 people who made their living commenting on political or economic trends. These were people in government and academia, not just the media.

He found that these experts were so bad at making predictions that you would have been better off just flipping a coin. Their predictions on yes or no questions failed to perform better than random chance. What was really striking was that they actually performed worse in their area of expertise than they did on general questions.

On general questions, they just picked the most obvious answers. But in their area of expertise, they had a pet theory they loved. And as they got more information, if the information supported the theory they accepted it. If the information contradicted the theory, they minimized, ignored or dismissed it. So as they got more information their confidence grew, but their knowledge actually shrank.

You know, on a day-by-day basis, the stock market apparently goes up about 54% of the time. So if you ask me to predict whether the market will go up or down tomorrow, I will absolutely always say “up”. Why? Then I’ll do better than a coin flip.

This isn’t a joke.

So that’s how predictable markets are. Meaning: If we want to invest well, we have to figure out how to do it while making no predictions of any sort.

Part 2: Trying to “out-perform” will cost you dearly

Predictions in investing normally come in three forms: market timing (attempting to guess whether markets will go up and down and moving in and out accordingly), stock picking (trying to guess which stocks will do better than others), or performance chasing (trying to find some “expert” who will do the above for you based on their track record).

None of these methods works, and the problem is that they are all expensive on top of being ineffective. Stock picking is the least expensive, which is probably why so many people stick with it. It’s also potentially the most dangerous, because any individual stock can blow up on you completely.

It also just doesn’t work. Here’s a picture of Luzsha the monkey. What’s her claim to fame? She was in a competition with 30 professional stock pickers, and she beat all of them. It’s just luck.

And yes, investing in the company you work for is stock picking. It’s stock picking of the worst sort, because you are stacking risk on top of risk. You already work for this company, and if it fails you’re going to be unemployed. Don’t stack investment risk on top of this! “But it’s a great company!” Yeah, that’s what Enron employees thought too.

One of the toughest things about being a financial advisor is convincing your clients to let go of their company stock, especially out here in Seattle, tech-land, where people still get these stock options they don’t want to let go of. They might have watched the stock price surge, and they don’t see that it can collapse just as fast. But I can say, in all my years working with people, no one has ever regretted selling their company stock.

On the other hand. A few people who ignored my advice came into my office for their next appointment with very sheepish looks on their faces. I always know exactly what that look means. “Lauren, we should have listened to you…”

Now we already know why market timing doesn’t work. It doesn’t work because predictions don’t work. So that leaves performance chasing, which is very popular because people want to believe that, somewhere out there, an expert exists with real magic.

Performance chasing is maybe the least dangerous way of trying to “beat the market”, but you can still lose a lot of money. A great example is the CGM Focus Fund. It was, in some sense, the most successful fund of 2000-2009 (which, by the way, was actually the worst decade ever for the US stock market.) The fund made an astonishing 18.4% per year. Someone who bought the fund in 2000 and held it until the end of 2009 saw their investment multiply by over five times!

The only problem is…no one actually did that. No one bought the fund in 2000 and just held it, because in 2000 the fund had no track record. Instead, people chased performance. They bought the fund after it went up, and then sold it after it went down. The investors in the fund didn’t make money at all–in fact, they lost 11% per year. They lost so much because the fund was incredibly risky, which meant that it did great when it did great, but crashed horribly when it did badly.

Now on average, people don’t lose THAT much by chasing performance. But numerous studies have shown that most active stock investors lose a little over 1% per year by constantly buying and selling at the wrong times, compared to what they would have made if they just bought their investment and held it.

And this is one of the true keys to investing–if it’s not worth holding forever, then it’s not worth buying at all.

In a world where returns might not be as high as they were in the past, you can’t afford to let market timing, stock picking and performance chasing chip away at your returns.

Part 3: If it sounds too good to be true, then it is too good to be true.

In some ways, you’ve just got to have street smarts. If you look around and CD’s are yielding one percent, and some sales guy is telling you about a variable annuity (or whatever) has a guaranteed return of 6%, you should know that there must be a serious catch. That guaranteed return isn’t guaranteed at all.

When someone sells you a product that says you can “participate” in the upside of the markets without having any possibility of loss, your street smarts should kick in. It isn’t going to be like that.

Here is the most basic, fundamental truth about investing. Risk and reward go hand in hand.

There is no such thing as an investment that just “produces income” without high risk. There is no way to get high returns, in any form, without high risks.

Looking at the most common investments, stocks and bonds, it’s as simple as this. Stocks have higher expected returns than bonds because stocks are riskier than bonds. If people could get the same high returns in bonds that they do in stocks without having to deal with the incredible volatility, then no one, really, no one would buy stocks. Everyone would just own bonds.

So the price of stocks is set low enough that they have high expected returns. Without those high expected returns, no one would invest.

And think about a bank loaning out money. Who do you charge a higher interest rate to, the low risk borrower or the high risk borrower? Of course, you charge a higher rate to the one who is the higher risk. Well, assuming both pay back their loans, who do you make more money off of? You make more money off of the higher risk case. But they are higher risk, which means you may not get your money back at all.

All of finance is like this. Flee–really, RUN–from anyone who tells you that you can get high returns or “income production” from low-risk investments.

You know what the scariest risks are? The scariest risks are the ones you don’t see. For instance, hedge funds can be frightening. Why? They don’t have to be transparent. They are allowed to estimate their returns if they invest in things that aren’t easily valued. This means they can tell you that they have steady returns, when they really don’t even know what their products are worth. This is why I strongly recommend investments like mutual funds, where you know exactly what you are invested in.

It’s very common for people to think they are avoiding risk when, really, they are just avoiding looking at it. Yes, the stock market goes up and down. You can see it. But your property values are always going up and down too. You just don’t always see it. Your family business has a value too. It’s worth something to somebody. That value is always going up and down. You just don’t see it.

The value of real estate and business constantly fluctuates, just like the stock market. Please don’t make the mistake that has bankrupted so many people. Don’t make the mistake of thinking stocks are riskier just because the risks are clear. Risk doesn’t disappear just because someone hides it from you.

Now there are things we can do to mitigate risk. We can diversify, which means we don’t put all our eggs in one basket. We can be smart.

But fundamentally, understand this. If you are not willing to take risk, then you are going to get incredibly low returns. In fact, you will probably get returns that barely keep up with inflation (or don’t keep up at all.) This leads us to point number four.

Part 4: Safety is an illusion.

With one important exception, there is no such thing as a safe investment. The reason it’s hard to see that is because of the inflation illusion.

Back in the seventies, you could get a savings account that paid double-digit percentages. Sounds great, right? The only problem was that when savings accounts were paying out 10% per year, inflation was floating along at 11%. So you see the problem? Technically, yeah, you’re making 10%. But in the real world of actual purchasing power, you are slowly but surely losing money.

Just like you should flee from people who promise high returns with low risk, you should flee from people who are trying to sell you “safe” investments.

There is one interesting exception to this rule. You can buy, directly from the US Treasury and at no cost, Treasury Inflation Protected Securities, otherwise known as TIPS. These are bonds that pay you a yield plus whatever inflation was over the time that you owned the bond.

The only problem? That yield might literally be zero.

So now you can focus your street smarts. The only investment on earth that is truly safe from inflation is an investment that, in the worst times, literally pays you absolutely nothing. That’s the true cost of safety–returns of exactly zero percent.

Part 5: Your financial “advisor” is not acting in your best interests.

So now that you know all this, the smart move is to get professional help, right? I mean, if someone’s gonna sue you, you get an attorney. If you have a complicated tax situation, you hire an accountant. I don’t try to do my own plumbing because I like not having catastrophes at my house. Why would anyone try to do their own investing?

The problem with hiring an advisor is that so many of them have a lot of sales training and not so much finance and tax training. Too many advisors still sell commissioned products, where the company they sell for pays them to prefer certain products over others. This is obviously not in your best interests. Other advisors, even if they are not on commission, seek to “add value” by trying to play with the big boys and using hedge funds or other odd strategies. This constant search for “new”, flashy investment strategies leads directly to performance chasing at best, and at worst it turns the advisor into a wanna-be Bernie Madoff.

Look, I’m a financial advisor myself so I don’t think the whole industry is corrupt. But most of the industry is either corrupt, foolish or badly misled. Honestly, too many financial advisors are like a doctor who smokes a pack a day and won’t exercise. And now they need you to finance their bad habits…

I could tell you all sorts of horror stories about my industry, but instead I’ll just say it like this. If you don’t know enough to invest on your own, then you don’t know enough to know if your advisor is acting in your best interests. It sucks. But it’s the world we live in.

I will also say this–flee from any “advisor” who sells out-performance. Really, just run. As an advisor, I can do a lot to help my clients form an investment plan that fits their goals, implement that plan, and then stick to that plan. What I cannot do is promise any sort of out-performance.

No matter whether you are doing it yourself or hiring a professional, chasing out-performance will eventually cost you. It will particularly cost you if you seek a professional to out-perform for you, because that professional has so much more exposure to garbage like hedge funds and other “alternative” investments where you can literally lose everything.

All of which brings up an interesting question. How do active mutual fund companies, hedge funds, and the Wall Street sales force survive at all?

Part 6: The media is REALLY not acting in your best interests.

How does active management survive? Primarily, the media. It’s the media that creates the illusion that predicting where markets are going and picking stocks is what investing is about. It’s the media that makes it seem as if experts, those same experts who cannot out-predict a coin flip, are really worth listening to.

And it’s the media that promotes the past performance of mutual funds without mentioning how many mutual funds had to fail outright in order for a few lucky ones to seem brilliant. Here’s a secret about active mutual funds. Companies set up, say, 10 mutual funds. Nine don’t do well. But after five years, one is lucky. Guess which one you hear about?

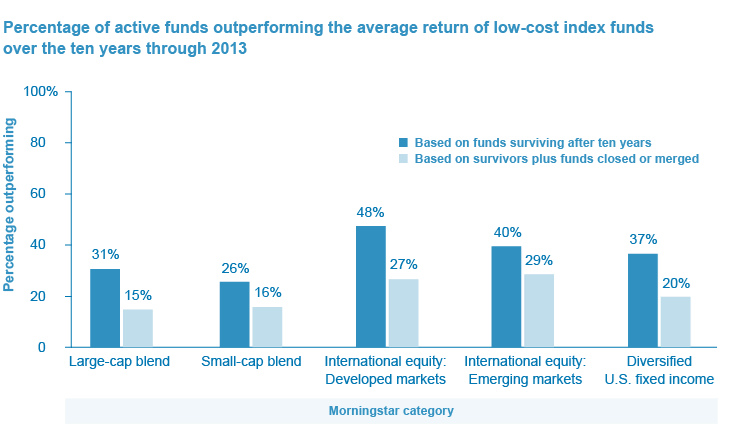

Here are the actual statistics. After one year, only 40% of actively managed mutual funds can beat their index (an index just represents the average return you could have gotten if you bought the market with no picking and choosing.) After 10 years, the percentage drops to 27%. And after 40 years, only 12% of actively managed funds can beat their index. That is a piss poor success rate, and it means you’d be better off throwing darts at a dart board to pick stocks than paying for “professional” management. (Or you’d be better off hiring a monkey, as long as the monkey didn’t charge much.)

But the really interesting statistic is the percentage of active funds that survive at all. After 20 years, half of all active funds have been shut down. And after 40 years, about two-thirds have been shut down. See? This is how they hide the terrible performance. They just shut the fund down, and act like it never existed in the first place. As long as the fund company starts enough funds, one of them will get lucky. That lucky fund will get sold to unsuspecting investors. The unlucky funds just disappear.

There’s a better way to invest. And not only is it better, it’s actually a lot simpler too.

Part 7: Boring investing works.

So what is that better way? We’ll discuss that in the next part, but let’s just get one basic truth about wealth building out in the open first.

Effective investing is boring investing.

Investing is how you preserve the wealth you build through your career or by starting your own business. But investing itself is not going to make you wealthy.

If you want to preserve and even build wealth, the best thing you can do is get out of the casino. Get yourself on a steady, automatic investment plan so you can focus on your career, your business, or your real estate. Or just spend time with your family.

Once you see how investing really works, you’ll see that you’re financially better off playing with your kids than trying to play the stock market.

Take the Class Exercises

Move on to the next class: Simple Investing

Return to the list of classes