Now that we know Wall Street doesn’t work, or at the very least, it sure doesn’t work for you, what does work?

Part 1: Passive investing and rebalancing

Alright, so we understand that market timing doesn’t work, monkeys are just as good as professionals at stock picking, and that the experts making predictions on CNBC are about as useless as a screen door on a submarine.

So what are we going to do?

We’re going to start by giving up on anything that requires predictions or stock picking, otherwise known as “active management”. Instead, we’re going to use passive management, which just means following simple, mechanical mathematical rules when investing. Instead of wasting time trying to pick stocks, we’re just going to own the whole stock market. Instead of trying to time the market, we’re going to own the market.

Here’s how it works. We’ll use index funds instead of actively managed funds. What are index funds? Well, for instance, there is a Total Stock Market index fund. If you buy it, you’re just buying the total US stock market. No picking and choosing. There’s also a Total International fund, which does the same thing for international stocks.

You can get index funds for small stocks, for the S&P 500 (the 500 largest US companies) and for almost any type of investment you might be interested in. And in your index fund, if Apple makes up, say, 2% of the total US stock market, then Apple will be 2% of your total stock index fund. If Bob’s Coffee is 0.00001% of the market, then it will be 0.00001% of your index fund.

No picking. No choosing. No predicting.

But the markets are still irrational and unpredictable. What do we do about the fact that markets go up and down, and that there are bubbles and busts? We’re going to handle the uncertainty and irrationality of the markets with rebalancing.

Rebalancing is not exciting, but it might be the most powerful tool available to individual investors. Let’s take an example. Say you are retired, and you have half your money in the stock markets and half in bonds. Let’s say stocks have a fantastic year, and bonds are pretty flat. As a result, you have made money, but your portfolio has also changed. Now, stocks are 55% of your portfolio, and bonds are only 45%.

Rebalancing means to return to the original balance. The original balance was 50% stocks and 50% bonds. So, you sell some stocks and buy some bonds.

What’s great about rebalancing is that it requires no predictive ability. It also allows you to stay in control of your portfolio. Meanwhile, as the years pass, you are not exactly selling “high” and buying “low.” You aren’t trying to predict the exact highs and lows of the market. Instead, you are selling higher and buying lower. And as those inevitable bubbles form, you are selling little by little out of the bubble. But you never sell out completely. And then, after the bubble bursts, you buy back in at lower prices.

Rebalancing is the most powerful tool in the passive investor’s arsenal because it eliminates the need for emotional decisions, it keeps you in control of your portfolio, and it mechanically forces you to buy at lower prices and sell at higher prices. It’s beautiful. And it’s boring.

But you know what? Your investing should be boring. Your life should be exciting. Your investing should be a stress-free way to build and maintain your wealth, so that you can focus on what really matters.

When you combine indexing with rebalancing, you are now completely in control of your portfolio, not some screwball Wall Street expert.

But maybe now it’s time to back up for a second, and just talk about the basics of investing. Everyone who reads this is coming from a different level of background knowledge, so now might be a good time to explain mutual funds, stocks, bonds, risk and return.

Part 2: Stocks, bonds and mutual funds

A stock is a piece of a company. If you own one share of Microsoft stock, then you own some very small percentage of the company Microsoft. If you bought all the Microsoft stock in the world, you’d own the company. Since you are a part owner of the company, you are entitled to dividends, your share of the company’s profits. And like any owner, you hope the company will increase in value over time so that, when you sell, you sell at a gain.

A bond is a loan. If you buy a Government bond, you are literally loaning our government money. If you buy a GE bond, you are loaning that corporation money. The yield on a bond is like the interest rate on a loan.

Bonds are much less risky than stocks. They also have much lower expected returns, and they have lower returns because they are less risky. As a matter of law, if a corporation goes bankrupt, first the bond-holders get paid off. If there’s any money left over (there won’t be) then stock-holders might get something. So stocks really are always riskier than bonds.

The risk of stocks is more than just that they go up and down a lot, although you should be aware that the stock market loses 10% or more so often that such a loss is merely called a “correction”. You know, like when your elementary school teacher corrected a mistake you made on a paper. It’s no big deal. It happens, on average, once per year!

No, the real reason stocks are risky is because when they go down, they go down at the worst possible times. It isn’t just random. When the economy is tanking, when unemployment is through the roof, when housing values are crashing, when your kids are begging you to move back in because they lost their jobs and they’ve got nowhere else to go, that’s when the stock market goes to hell.

Now you can mitigate a whole lot of this risk through diversification, by not putting all your eggs in one basket. If you own thousands of stocks, and one of them turns out to be Enron, you’ll be fine. But you probably aren’t rich enough to own thousands of stocks if you have to put together your own portfolio. I mean, most people aren’t that rich.

So what’s the solution? Mutual funds. In a mutual fund, people pool their money together and hire an advisor, which is the mutual fund company, to put together a diversified portfolio of stocks, bonds, or other investments. The mutual fund company, though, does not own the fund. The investors own the fund. If the mutual fund company fails, you don’t lose any money. A different company will simply have to take over the job of running the fund.

Mutual funds have what are called “expense ratios”. This is the money paid every year to the company so that it will run the fund. Index funds often have very low expenses. It’s not rare for index funds to have expenses of less than 0.1% per year. On the other hand, active funds usually have expenses of 1% or more. You can immediately see why so few active fund managers can add any value!

Finally, mutual funds are completely transparent and regulated by the SEC. They have to report their holdings and they have to report the current market value of everything they own. This makes them radically different from hedge funds, which often are allowed to estimate the value of their holdings are which are not nearly as well-regulated. So Bernie Madoff, for instance, could never have stolen from people if he had been running a mutual fund.

Stock mutual funds are probably the greatest wealth growing tool available to the world’s middle class in all of history. Their transparency, efficiency and utility in passive investing strategies makes them perfect for most of you who are trying to achieve financial independence.

And if you choose to use index funds and a passive strategy, there is another wonderful benefit to mutual funds. It’s easy to diversify your portfolio, and that diversification is the best tool you have to mitigate risk.

Part 3: Diversification

In finance, diversification has a very specific meaning. A diversified portfolio is one where the investments don’t go up and down at the same time together, or to the same extent. So if you have 500 investments, but they all move in lock step, then you are not diversified. On the other hand, using mutual funds, you can achieve a reasonable level of diversification with as few as three broad investments.

The first step is, of course, don’t put all your eggs in one basket. You can avoid the Enron problem simply by making sure you at least use a total market index fund. Now you have the whole US stock market in your portfolio.

But in some sense you are still putting all your eggs in one basket–and that basket is the United States. It’s better to invest internationally as well, just in case the US stock market has a long period of terrible performance.

Remember that, if everyone expects the US economy to be an 8 on a scale of 1 to 10, and instead it’s a 7, then stock returns will be poor. Believe it or not, after inflation is considered, the US stock market’s performance from 2000-2009 was the worst decade ever. There was no decade in the Great Depression when stocks did as poorly.

Why?

If anyone remembers the late nineties, you might remember the magazine covers with headlines like, “Everyone is getting rich except me!” You might remember day traders borrowing money on credit cards to play the stock market. You might even remember when “experts” were claiming that risk had disappeared from investing.

Well, with that much irrational optimism floating around like a smoke bomb, risk came back with a vengeance. No economy could have kept up with the ridiculous expectations created by Wall Street and the media in the late nineties, and to make things worse, we replaced a tech stock bubble with a real estate bubble just a few years later.

An even better example is Japan. Does anyone remember the late eighties, when Japan was going to buy everything? They were on top of the world. Their stock market reached such a bubble that, after it burst in the late nineties, a quarter of a century later it was still down. In fact, it was so bad that a Japanese investor who put all their money in their home country’s stock market would have lost, in Yen, 80% for decades.

When I say stocks are risky, I mean they are risky.

It’s true that international stocks are riskier than US stocks, because they include emerging markets like China and Russia. However, the combination of international stocks and US stocks is less risky than just owning US stocks alone, because US markets don’t always move in lockstep with Chinese markets.

I remember so clearly in the late nineties thinking, “OK. Japanese stocks have been down forever, but they just have to go back up now!” I was wrong. And I can stand to be wrong by a few percentage points in some years, but I couldn’t live with myself if I recommended to people that they should put all their investments in US markets, and then US markets pulled a Japan.

Remember. Japan is still rich! They’re still an economic powerhouse. But their markets performed horribly for decades. And by the way, yes, a Japanese investor who had chosen a global portfolio would have made money over the same period that their own stock market’s prices collapsed. Just like a US investor from 2000-2009 would have made money with an international portfolio, even during the worst decade ever for the US stock market.

In other sections we’ll go into more and more detail about diversification among stocks, and how to diversify into small and value. For now, though, let’s talk about the bedrock of most investors’ portfolios, the diversification between stocks and bonds.

Part 4: Your risk tolerance

Stocks and bonds are a great combination, particularly for retirees, because their returns are so uncorrelated. In fact, it’s better than a lack of correlation. Often during serious bear markets investors pour money into bonds as stock prices crash. As a result, bonds often have their best years precisely when stocks have their worst years.

Since stocks have high risks and high returns, and bonds have low risks and low returns, you can set up a risk/return profile to match your own exact tolerance for risk. This is one of the many benefits of passive investing. It leads to simple, answerable questions. How much do you want to invest in stocks, and how much in bonds?

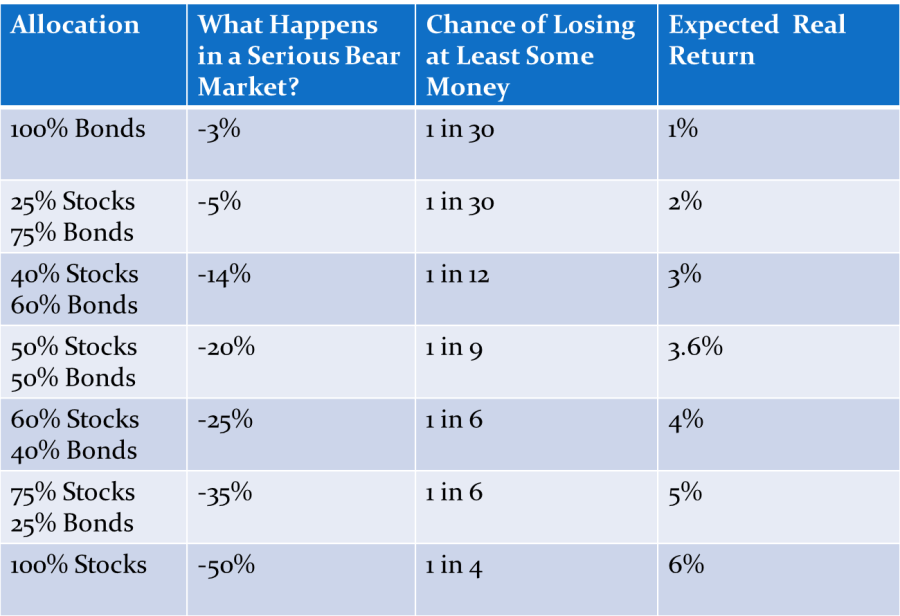

It’s true that, on average, younger investors are more aggressive and older investors are more conservative. But this is just an average, and you might be very different. Here is a table to help you decide on your own risk tolerance.

The table there shows the percentage of the portfolio you might have in stocks and bonds, the expected real (real means inflation-adjusted) returns of the portfolio, and your chances of losing at least some money in any given year. The table also shows how much you could lose in a “really serious bear market” like 2009, 2000-2002, or 1973-74. (A bear market is any time the stock market loses more than 20%. I have made up my own definition of “really serious bear market” which is when the stock market drops by half or more.)

Please notice how often a 100% stock portfolio loses at least a little bit of money! Also, please notice how little additional risk you are taking when you move from 100% bonds to including a small portion of stocks in your portfolio. It really isn’t worth it for most people to try to be too safe.

One of the nice things about simple investing is that it allows you to focus on a small list of really important decisions. If you decide to invest simply, determining your own risk tolerance is one of those important decisions. And, from many years of experience, I would suggest thinking of risk in real dollars, not just percentages.

So when you check out those numbers for bear markets, remember to translate those percentages into actual dollar losses. Otherwise, you may think you can tolerate more risk than you really can.

Most people have a pretty good idea of how aggressive or conservative they are. And you can tell just by looking at a table like this where you stand. Trust yourself.

Part 5: Keep it simple and stay the course.

Do you want to keep your investing simple? If so, I have some good news. At Vanguard, a company that has become the largest mutual fund company on earth by committing to low-cost, passive investing, you can get the basic level of diversification everyone needs in one fund. And they’ll rebalance it for you.

The funds are called Lifestrategy and funds, and you can read about them here.

This is the simplest investing strategy on earth, and it works. These Lifestrategy funds are funds of funds, which means they contain other Vanguard funds and rebalance those funds regularly. The Lifestrategy funds contain the Total US Stock Market Index, the Total International Stock Index, the Total Bond Index and the Total International Bond Index.

Are you interested in a fund that will slowly reduce your stock allocation as you age? Well, on that same page you can find a link to Vanguard’s Target Retirement funds, which do just that.

With either the Lifestrategy or the Target Retirement funds, you don’t have to do anything besides set up your account. From then on, Vanguard does all the work for you. Investing could not be simpler.

Are these the absolute best possible funds for you? Well, probably not. But I bring this up to show you how simple investing can be if you want it to be simple. Here is a one-fund solution that includes a global portfolio of stocks and bonds, rebalanced consistently, adjusted to your risk tolerance. It may not be perfect, but here is an uncomfortable truth. If a simple fund like this won’t get you to your financial goals, then a more complex form of investing probably won’t either.

Furthermore, the story you can tell yourself about why you are investing the way you are is both elegant and powerful. You are investing in the economic potential of the entire globe. That’s it. That’s what you own. You own the expected returns of the economic growth of the entire world, and that is really a great place to be. Up until the last few decades, only the richest people on earth could own a portfolio of the world’s stocks and bonds. Now that same global portfolio is available to any investor with a few thousand dollars to put to work!

As I said, there are more mathematically optimal methods of investing than the simplest option, and I talk about them in the sections on Retirement Investing and Maximize My 401k. But there is one big advantage to simple investing, and please don’t underestimate how powerful this advantage is. Simple investing makes it easy to stay the course.

To quote my hero, Jack Bogle, “The three most important words in investing are: “Stay the course.” All this stuff about expected returns and diversification doesn’t mean diddly if you don’t keep invested.

And you need to keep invested because, in the long run…

Part 6: Optimism

In the long run, only optimism is rational.

Because of the fact that economic growth is gradual, it’s easy to lose sight of what it really is. Economic growth IS growth in knowledge. And that growth in knowledge has unambiguously made our lives better.

If you want to see what economic growth really is, don’t follow the money. Follow the people. Follow the actual goods and services. Follow the massive improvements in public health and public education. Most of all, follow the almost unimaginable increases in knowledge.

I am not exponentially richer than my great-grandparents because of money. I am exponentially richer than they are because what I take for granted, they couldn’t have even imagined.

I have, on my desk in my office, an adding machine that accountants used to use in the 1950’s. It can add and subtract. It weighs a ton. I can’t imagine carrying it around anywhere. What is economic growth? Economic growth is the difference between that adding machine and my Excel spreadsheet.

Have you ever looked at photos of those old computers that NASA used to use? You know, right, that your smart phone contains more computing power than every computer NASA had when we landed a man on the moon for the first time? That’s economic growth, and it isn’t going anywhere.

If you really want to see it, look at the enormous reduction of global poverty over the last 200 years. In 1820, over 90% of the world’s population was living in extreme poverty. Today, the percentage is about 10%. And progress continues. Right now, every second, three people escape poverty globally. And where are they going? They are joining a massive and growing global middle class.

In 1980 there were fewer than 300 million middle class people in the world. Today, there are well over 2 billion. If anyone likes, they can feel free to quibble with the definition of middle class. It doesn’t matter. Choose any realistic definition you want, and you’re going to come up with similar results. The global middle class today is somewhere between 6 and 7 times as large as it used to be, despite the fact that global population growth has been consistently slowing since the 1960’s.

You want to know why you should invest? You should invest because that’s the easiest way to get a piece of the wealth created by that 2 billion strong global middle class.

Or look at improvements in public health. In 1900, 40% of children did not live past age 5. Today, infant mortality has declined to a mere 4.3%, and this includes the poorest areas of the world. We are living longer and we are eradicating new diseases every day. Here’s something the media rarely reports–we’re even doing a good job battling against Alzheimer’s and dementia. From 2000 to 2012, the percentage of older Americans with dementia declined from 11.6% to 8.8%. The risk of dementia has been falling by 20% every decade since the late 70s, and this decline in dementia is occurring in every developed nation.

Long-term optimism is the only form of long-term thinking that is rational. So as soon as you have your spending and saving in order, get out there and start investing. You want to give compounding as much time as possible to work for you, and there is no reason to sit on the sidelines while the rest of the world creates unimaginable wealth.

Take the Class Exercises

Next Up: Learn how to maximize your 401k or Learn about Investing in Retirement.

Return to the list of classes