“Lauren, how do I get the most out of my 401(k)?”

This might be the single most common specific question I hear when I meet with people. For most of you, the primary vehicle through which you will invest money is some sort of a 401(k) plan. But if you do not have one and are building an investment strategy on your own, then the discussion here will still help you get the most out of your investments. You can easily apply the lessons here to creating your own portfolio at Vanguard, or to choosing an ethical financial advisor.

So whether you are using your company’s 401(k) plan or doing it yourself, here are the steps to success.

Part 1: Save future raises

The longer I work in this business the more convinced I am that there is exactly one correct method of increasing savings in 401(k) plans. People should save their future raises.

Too often when people try to jump into 401(k) plans they end up making things worse because they go into debt by the exact amount that they are saving! This is madness. It’s much better to save your future raises because then you won’t ever get that bump up in lifestyle (which probably won’t make you one iota happier anyway) and so you’ll never get used to spending more.

Now if your company offers to match your investments in a 401(k), then by all means, get the match. Other than that, save your future raises. Your future self will be eternally grateful.

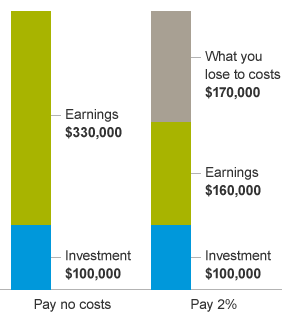

Part 2: Use low cost funds

Expenses eat away your investment returns. Look for the funds that have a low expense ratio. Use passive funds if you can. Exchange traded funds, funds labelled index funds and funds from Vanguard are usually going to be good choices.

It should be pretty easy to find the expense ratio of the fund. That’s one of the most important things your plan has to list. Also, when it comes to stock funds, look for low turnover. Turnover is a measure of how often the fund trades its portfolio of stocks. The higher the turnover percentage, the more often your mutual fund is churning your portfolio.

If a fund has turnover of more than 50%, that is a real danger signal. That means that over half the portfolio is being replaced over the course of a year. Why are they trading so much? Do they have a real strategy, or are they just guessing? And on top of those questions, it does cost some money to trade. And the costs of those trades are coming out of your returns.

Keep costs and turnover low, and in the long run, you’ll get to keep more of the returns for yourself.

Part 3: Diversify into small and value

Here is where things get tricky, so we’re going to spend some time on this subject of small and value..

For years, people tried to figure out what caused different stocks to have different returns. As it turns out, the over-powering majority of stock returns are explained by three factors: market, size, and value. In other words, US stocks often have very different returns than stocks from other countries. Stocks of big companies have different returns from stocks of little companies. Those two factors are easy to explain.

The harder factor is value (or value vs. growth.) A value stock is a stock that has a low price relative to its book value or its earnings. A growth stock is a stock that has a high price relative to its book value (or earnings.)

The difference between the returns of the US market and the market of, say, Brazil, is easy to explain. Brazil’s stock market is riskier and it has higher expected returns. Easy. Same with small companies and big companies. Small companies are riskier and have higher expected returns than large companies. Another way to look at it is that small stocks have a lot more room to grow than large ones do, but they also have a much higher chance of not making it at all.

With value and growth, it’s a lot more annoying to explain. Value stocks are riskier than growth stocks and have higher expected returns. Yep, growth stocks have lower expected returns. I know. It doesn’t make sense. I wish they hadn’t called them “value stocks” and “growth stocks.” I wish they called them low-priced stocks (value) and high-priced stocks (growth.) Then it would be easier to see the risk story.

Why do those value stocks have high risks and high returns? Well, why is the price low? There must be something causing investors to stay away from that stock. Of course, maybe investors avoid value stocks just because they are boring old companies that sell diapers and soap, and they over-price growth stocks because those companies are shiny exciting companies like Amazon. It might be both a risk story and a little bit of something else.

Whatever the case, value stocks have historically had higher returns than growth stocks. But what’s really good about these three factors is that the risks don’t always show up at the same time. Japanese stocks and US stocks don’t always go up and down together. Small stocks and big stocks don’t always go up and down together. Neither do value and growth.

So you can really benefit by diversifying.

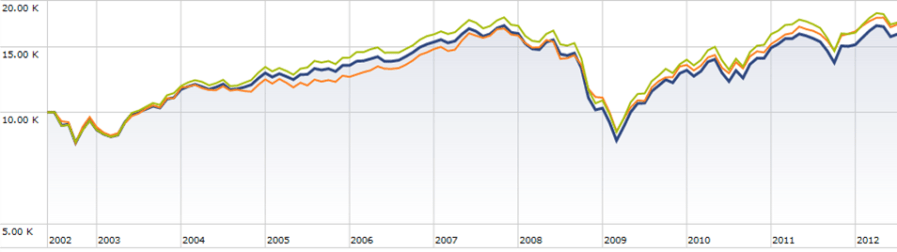

Here is a chart of the 10 year performance of the Dow Jones Industrial Average of the 30 largest US companies. There is also on the chart the performance of the 500 largest US companies, which make up the S&P 500 index. Then, we have the performance of the total US stock market–every single stock.

At one point in 2012 I made this chart just to see how it would look. And lo and behold, you can barely tell the difference between the three lines! They are almost exactly the same! They don’t just end up in the same place. They travel almost exactly the same route to get there. This happens because the largest US companies are SO big that they just dominate the returns of the US stock market.

So this is why it’s become so popular to divide stocks into small and large (and mid), value and growth (and “blend”). You may also see the word “cap”, which just means “capitalization”. So small cap just means small capitalization. With this information, you can now tell what those fund names in your 401k actually refer to. Useful, no?

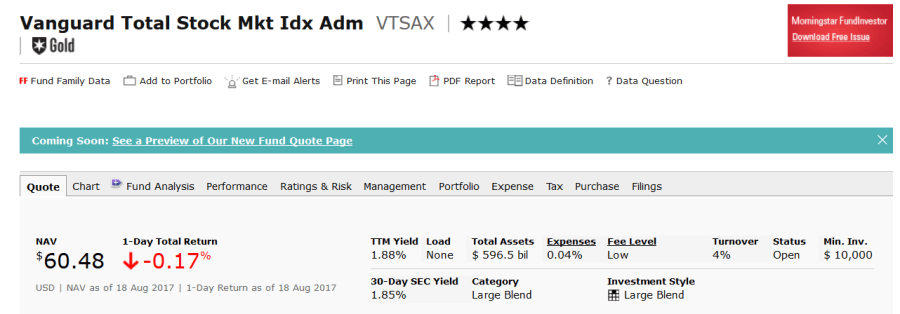

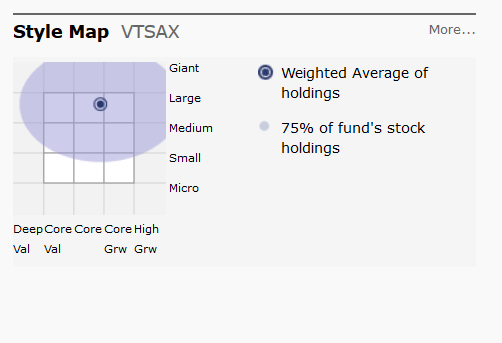

Here is a sort of box that you may see a lot, especially if you look up your funds on morningstar.com.

If you look up a fund on morningstar, or yahoo, or some other site, it will usually present you with a box similar to the one above. Then it will place a dot on the box. That dot shows you, in the grid of value and growth, where your fund is located. It’s really handy, actually, because you can see how different your funds really are.

If you’ve got 10 funds, but they’re all in the same place on that box, you really aren’t diversified. You’ve just got a bunch of complexity.

Side note: I strongly advise you to ignore any form of “star ratings” when using sites like morningstar. However, such sites are very useful simply to learn about the funds you have in your 401(k).

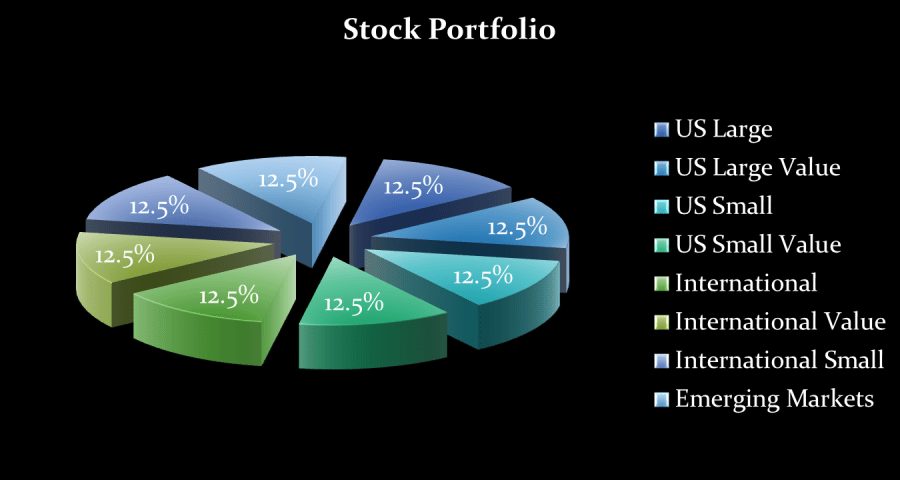

I suggest diversification over complexity. Here is a model stock portfolio:

Notice the portfolio has 8 different types of stocks, and is divided evenly. That’s pretty much it. In the past, this portfolio has delivered superior risk-adjusted returns to a simple US stock market portfolio. Since 1972, the portfolio above has had real returns of 8.2% per year, while the US stock market returned 5.9% real. The worst years for each portfolio were similar–the risk was basically the same either way.

That’s a pretty big difference in returns. I don’t necessarily expect that the future to be so good to the diversified portfolio, but I do believe that you are better off with a more diversified portfolio than with a portfolio that is basically mimicking the performance of the 30 largest US corporations.

Now if you are doing your own investing, it’s not too hard to set up this portfolio on your own. You decide how much you want in bonds, and then split up the stock section of the portfolio evenly. So if you want 20% of your money in bonds, then you put 10% in each stock asset class. If you want 60% of your money in bonds, then you put 5% in each stock asset class. And so on. You can easily use vanguard funds to set up this portfolio, or you can use ETFs.

But what if you’ve got a 401(k) plan? You don’t necessarily have a perfectly diversified set of options in a 401(k). So how do you set up such a portfolio?

My suggestion is that you look through your funds and see how close you can get to each of the asset classes I mentioned. So for instance, maybe your 401(k) has no Small Value fund. But maybe it has a Mid-Cap Value. Use that. Your plan probably has no International Small fund, but maybe it has an International Real Estate fund. Basically, using the idea of the “style box” in the picture above, you can try to get as close as possible to an ideal diversified portfolio.

And in any case, there is no perfect portfolio. We don’t know the future. The suggested portfolio even has a compromise because of the way international funds are set up–that’s why it has a separate allocation to Emerging Markets. So I wouldn’t be too worried if you are missing out on one or two asset classes.

The key is to avoid having 10 funds that all do exactly the same thing, and to avoid funds that use strange strategies that no one really understands. Most people don’t stay at their jobs forever anyway, and when you leave your job you can roll your 401(k) over, tax free, into your own IRA. That IRA can be invested however you’d like. (If you have plans from previous employers just laying around, it would be wise to roll them all over into one IRA that you manage yourself. This can be easily done at Vanguard or with any competent financial advisor.)

Until then, you do have a choice–should you go with the more complex portfolio I’ve listed above? Or would you be better off with something simpler?

Part 4: “Should I use balanced funds or target date funds?”

They are your simplest option and in many cases are often the best option for a starting investor. This question is hard to answer because there is such a range of balanced and target date funds, and some are much better than others.

The general answer, though, is that they are just fine for anyone starting out. But as time goes on, you will see that you are better off if you learn about how investing really works and make your investments really work for you.

Part 5: Further resources

For many of you, now is a great time to get more educated on how markets work. I highly recommend visiting the Bogleheads forum and asking about your 401(k) plan, or asking about any other financial questions you may have. I also emphatically recommend their reading list. (You can even find the book there that I wrote a chapter in! Yay!) If you just want to talk to a human being about all this, feel free to email me.

I think everyone needs to read one good book about investing. Websites and blogs are great, but it really helps to get immersed in the subject at least once. Your investing might be the difference between a stress-free retirement and a life-time of worrying about money. It’s worth it to spend the time to read one solid book.

For now, though, if you are just starting out, the important thing is to return to point number one: save your future raises. Get in that habit, because you won’t be young forever, and your 75 year-old self wants to have fun too.

Take the Class Exercises

Move on to the next class: Investing in Retirement

Or: Find out how much you need to be saving now.

Return to the list of classes