“Alright Lauren, I get it. I need to invest. But look, how much do I need to invest? How far behind the eight-ball am I? Am I going to eat dog food in retirement?”

Normally when I meet with people this is the number one question they have. Obviously, no one can give you an absolute answer, but we can figure out whether or not you are basically on the right track. The first step will be the hardest…

Step 1: Figure out how much you are spending per month.

This one’s easy to explain although it might not be fun to actually do. Download your bank statements from the last two months. Figure out how much you spent.

Now assuming that wasn’t too painful…

Step 2: Estimate how much you will spend per month in retirement.

Now look at your expenditures. Which ones do you already know will change when you’re retired? Alright. Cut those out and find out how much monthly spending is still left. That’s your estimate of retirement spending. It’s just an estimate and it’s good enough.

Side-note: Will life be different when you retire? Of course! But it’s still worth it to get an estimate, because this method is going to get you a much better answer than some weird number that doesn’t apply to you, like “you need a million dollars!” Or, “You need to replace 60% of your pre-retirement income.” Yeah, whatever. Let’s start by at least trying to find out how much you’re actually going to spend.

Step 3: Figure out how much your portfolio needs to provide.

So you’ve got your monthly spending number. We’re going to do all of this in today’s dollars, so that will make things easier. Check out your Social Security statements and get a reasonable estimate of how much Social Security will pay you per month. Alright, subtract the SS payments from your spending estimate.

Great. Now you have the monthly income that your investments will need to provide.

Multiply this number by 12 to get a yearly total.

We know that, historically, 4% has been a safe withdrawal rate for yearly withdrawals. (If you’d like to see the justification for this 4% number, look here.) So your portfolio needs to be big enough that it can handle a 4% withdrawal. Another way of saying that is that the portfolio needs to be 25 times the yearly withdrawal (this is algebra). Therefore, multiply your yearly total by 25 to get the ideal portfolio size that you should shoot for in retirement.

Let’s use a concrete example to show the math.

Let’s say you figure your monthly income need will be 5k. SS will provide 2.5k. Now you’ve got a 2.5k difference here that needs to be made up. That’s what your portfolio has to pay you in retirement. Multiply that by 12, and you get 30k per year. Your yearly portfolio withdrawal will be 30k, and so you want a portfolio where 4% of the portfolio equals $30,000.

$30,000 is 4% of $750,000. If you want to do the math easily, multiply 30,000 by 25 and you get 750,000.

Now use your own numbers, your real spending numbers, and figure out what portfolio size you’re aiming at. You might be surprised by how high (or how low) your number is. It doesn’t matter. It’s your number.

Next we have to figure out how much your investments can expect to make between now and retirement, and then we can figure out how much you need to save.

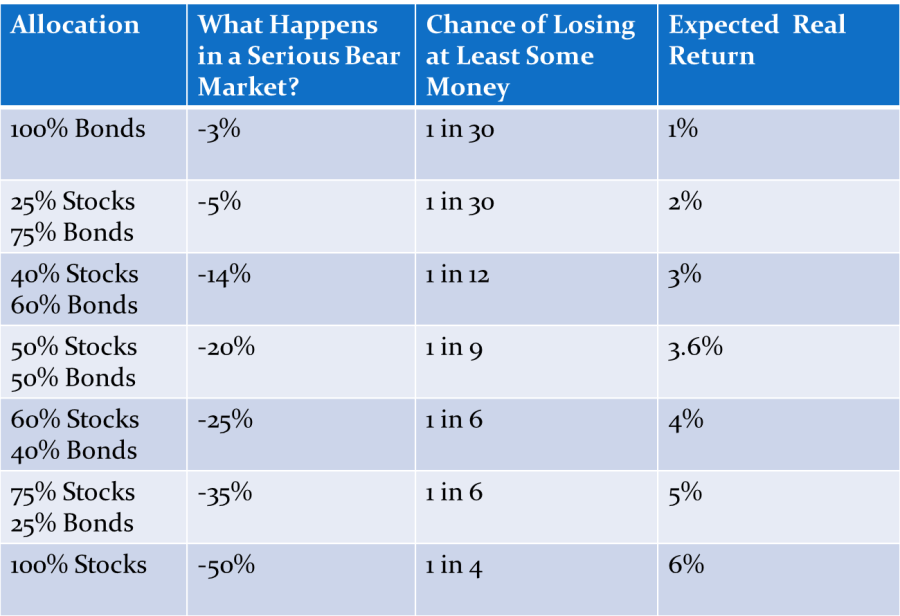

Step 4: Expected returns

Once again, we’re doing this with inflation-adjusted numbers. (“Real returns” means inflation adjusted returns.) So here are the expected real returns that I’m going to suggest you use:

Now it’s time to get out the Excel spreadsheet.

Step 5: Guess and check

I suggest using “guess and check” first. Basically, you want to start off by looking at how much you are saving now, and see where you end up. Then figure out, through guess and check, how much you really should be saving. This is a slower method of doing the math, but I think it will help you visualize how much things need to change for you to get where you need to be.

(Since this is difficult for most people to do merely by reading instructions, I have recorded a video here to help.)

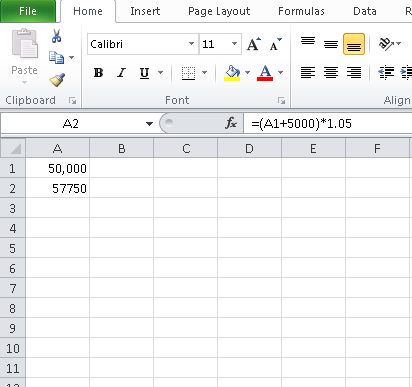

In the first cell of the spreadsheet, I want you to put in the amount you have invested so far. Let’s say it’s 50,000. And let’s say you are going to save 5,000 per year. Let’s say you are using a 75% stock portfolio. The stock portfolio then has expected returns of 5% per year. So each year, we will multiply the portfolio value by 1.05 (Or, by 105%, which is mathematically the same as saying the portfolio went up by 5%.)

So in cell A1 is 50,000. In cell A2 is the following formula:

=(A1+5000)*1.05

It should look like this:

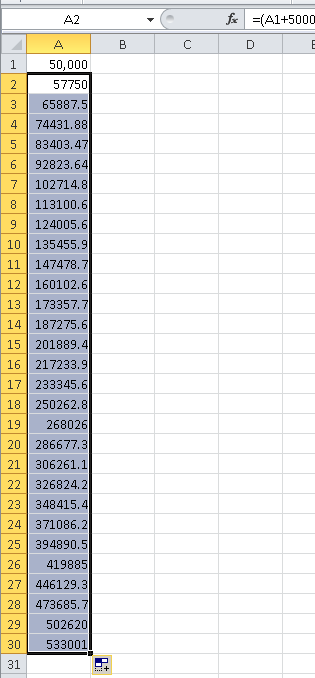

Now, how many years until retirement? Let’s say 30 years. Go ahead and grab the corner of the A2 cell and drag it down 30 rows so that the formula repeats 30 times. Where did we end up?

With this hypothetical example, we ended up at a little over 530k. That’s not going to do it. We had just figured out that our hypothetical investor needs a portfolio value of 750k at retirement. So now, let’s adjust that savings number until we find out how much we need to save.

Let’s try 6,000 per year. Nope, that’s not enough. It gets us to about 600k. How about 7,000? Still not enough. 8,000? Almost! It looks like our hypothetical investor needs to be putting away about $8,500 per year to reach the goal. That’s a pretty big bump up in savings, but not impossible.

OK, now try it with your own numbers.

How close are you? What did you learn?

Step 6: Why not more detail?

Why don’t I suggest more detailed financial planning?

Because, in simplest terms, life happens. Careers change. Relationships change. Goals and ambitions change. More complex, detailed financial planning can give a greater sense of comfort but doesn’t always align any more closely with reality.

Now you can certainly try to get a little bit closer to reality if there are certain things that you absolutely know will happen, and that these things will change the results. That’s perfectly fine. Some of us walk a more predictable path than others.

But I mean, really, what we need to know is your death date. That’s what would allow us to perfect the financial planning process! So just get that all figured out and then we can plan your life down to the second. But we don’t know that, or anything else that’s at least as critical, so I think this “back-of-the-envelope” planning is the best we can do.

So what did you discover? Are you on track or not?

Take the Class Exercises

Move on to the next class: Entrepreneurship and Rental Properties

Return to the list of classes